Download StrategyQuant X Ultimate Build 133 – Advanced Algorithmic Trading Strategy Development

StrategyQuant X Ultimate Build 133 is a specialized algorithmic trading strategy development platform, engineered by StrategyQuant to automate the creation, evaluation, and optimization of trading systems. This sophisticated software empowers quantitative developers, institutional traders, and financial researchers by offering advanced genetic programming and machine learning capabilities. It is designed for use within the financial trading industry, catering to sectors such as quantitative trading, hedge funds, and financial research, with support for a wide array of asset classes like Forex, stocks, futures, and cryptocurrencies.

Overview of StrategyQuant X and Its Role in Algorithmic Trading

StrategyQuant X serves as a comprehensive solution for developing automated trading strategies, addressing the complex demands of modern quantitative finance. Its foundational technology combines genetic programming with machine learning, enabling users to generate, test, and refine trading algorithms without the need for extensive programming expertise. The platform is instrumental for professionals seeking to leverage data-driven insights for market participation, providing robust tools for strategy discovery and validation essential in volatile financial markets.

Automated Trading Strategy Generation Using Genetic Programming and AI

The core innovation of StrategyQuant X lies in its fully automated strategy creation engine. It employs genetic programming, a subset of artificial intelligence, to evolve trading rules and parameters through simulated natural selection. Machine learning algorithms further refine these strategies by identifying complex patterns and correlations within historical data. This approach allows users, even those without deep programming backgrounds, to visually construct and iterate on potent trading algorithms, significantly accelerating the development cycle.

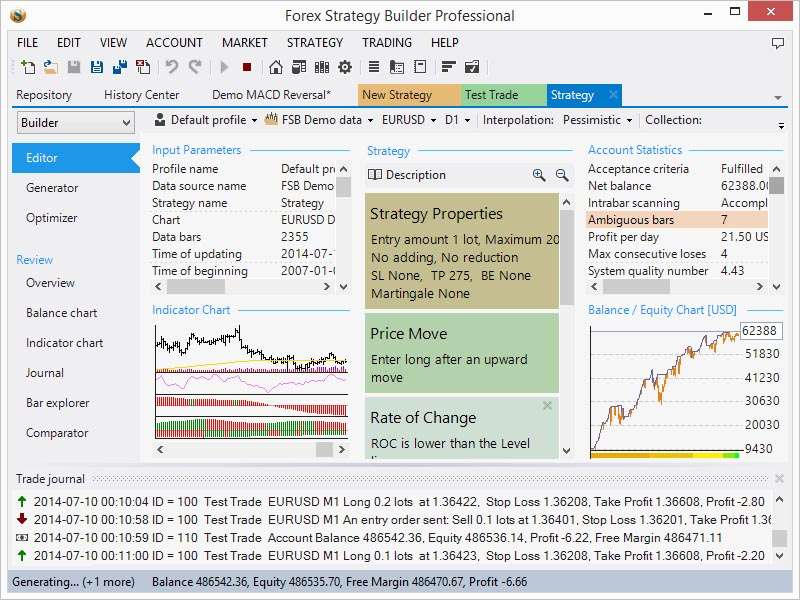

Comprehensive Backtesting and Robustness Validation Techniques

StrategyQuant X features a powerful backtesting engine that meticulously assesses the historical performance of generated trading strategies. This engine utilizes extensive historical data across various markets and timeframes to simulate trading execution, calculate key performance metrics, and identify potential profitability. Crucially, the platform integrates advanced techniques for robustness validation, including out-of-sample testing and walk-forward analysis, to ensure that strategies perform consistently under diverse market conditions and are not merely curve-fitted to historical data.

Advanced Risk Management and Portfolio Optimization Tools

Build 133 introduces enhanced risk management functionalities aimed at ensuring the stability and profitability of trading operations. The software provides sophisticated tools such as Monte Carlo simulations to assess potential worst-case scenarios and robust position sizing algorithms to manage capital effectively. Users can implement portfolio-level controls and risk mitigation strategies, allowing for the development of trading systems that are not only profitable but also resilient to market volatility and drawdown, a critical aspect for institutional trading environments.

Multi-Market and Multi-Asset Support with Visual Analytical Tools

Designed for broad applicability, StrategyQuant X supports a wide spectrum of financial markets and asset classes, including Forex, stocks, futures, and cryptocurrencies. It accommodates various trading timeframes, enabling comprehensive analysis irrespective of market type or trading style. The platform integrates advanced visual analytical tools, such as charting and performance visualizations, which provide users with clear, intuitive insights into strategy behavior, risk profiles, and potential performance across different market conditions.

Improvements and New Features in Ultimate Build 133

Ultimate Build 133 of StrategyQuant X incorporates significant enhancements focused on elevating performance and user experience. This release features refined AI algorithms for more accurate strategy generation, expanded support for a wider range of assets and markets, and improvements to the user interface for greater ease of use. Furthermore, computational efficiency has been optimized, leading to faster strategy generation and backtesting processes, enabling quantitative traders to analyze more scenarios in less time.

Use Cases and Application Scenarios in Professional Trading

Hedge funds and quantitative trading firms leverage StrategyQuant X for systematic alpha generation, utilizing its automated approach to discover and deploy statistical arbitrage, trend-following, and mean-reversion strategies. Financial researchers employ it to test hypotheses and develop new trading methodologies. Retail traders, including day and swing traders, benefit from its no-code interface to create and validate their own custom trading systems, integrating advanced risk management principles into their daily operations and strategy innovation.

Frequently Asked Questions

How does StrategyQuant X create trading strategies without programming knowledge?

StrategyQuant X utilizes advanced genetic programming and machine learning algorithms to automatically generate and optimize trading strategies through a visual interface. This process allows users to build complex trading logic and parameters by defining market conditions and desired outcomes, rather than writing traditional code, making sophisticated strategy development accessible to a wider range of traders.

What types of financial markets and assets does StrategyQuant X support?

The software supports multiple asset classes including Forex, stocks, futures, and cryptocurrencies, allowing users to develop and test strategies across diverse markets and timeframes. This broad compatibility ensures that professionals can apply StrategyQuant X to their specific trading interests, whether they focus on liquid futures markets or emerging cryptocurrency assets.

What risk management tools does StrategyQuant X include to ensure strategy robustness?

StrategyQuant X offers advanced risk management features such as walk-forward analysis, Monte Carlo simulations, out-of-sample testing, and position sizing tools to validate and optimize trading strategies for real-world conditions. These comprehensive tools help traders rigorously test their strategies against various market scenarios, mitigate potential drawdowns, and build more resilient trading systems.

Reviews

There are no reviews yet.